Securing Your Golden Years: An In-Depth Look at the LIC Jeevan Shanti Pension Plan

Introduction to LIC Jeevan Shanti

Retirement planning in India is often synonymous with long-term, reliable instruments, and the Life Insurance Corporation of India (LIC) has long been a trusted name in this space. The LIC Jeevan Shanti Plan (Plan No. 858/859 – formerly 858, now often referred to as New Jeevan Shanti 862 or updated versions, but retaining the core deferred annuity structure) is a standout single-premium annuity product designed to provide a secure and guaranteed income after retirement.

For an Indian reader searching for a stress-free retirement, this single-premium LIC Pension Plan offers a lifetime of fixed income, eliminating market risk and providing the much-needed financial stability in later life. This detailed guide breaks down everything you need to know about this popular LIC Annuity Policy.

Key Features and Plan Options of LIC Jeevan Shanti

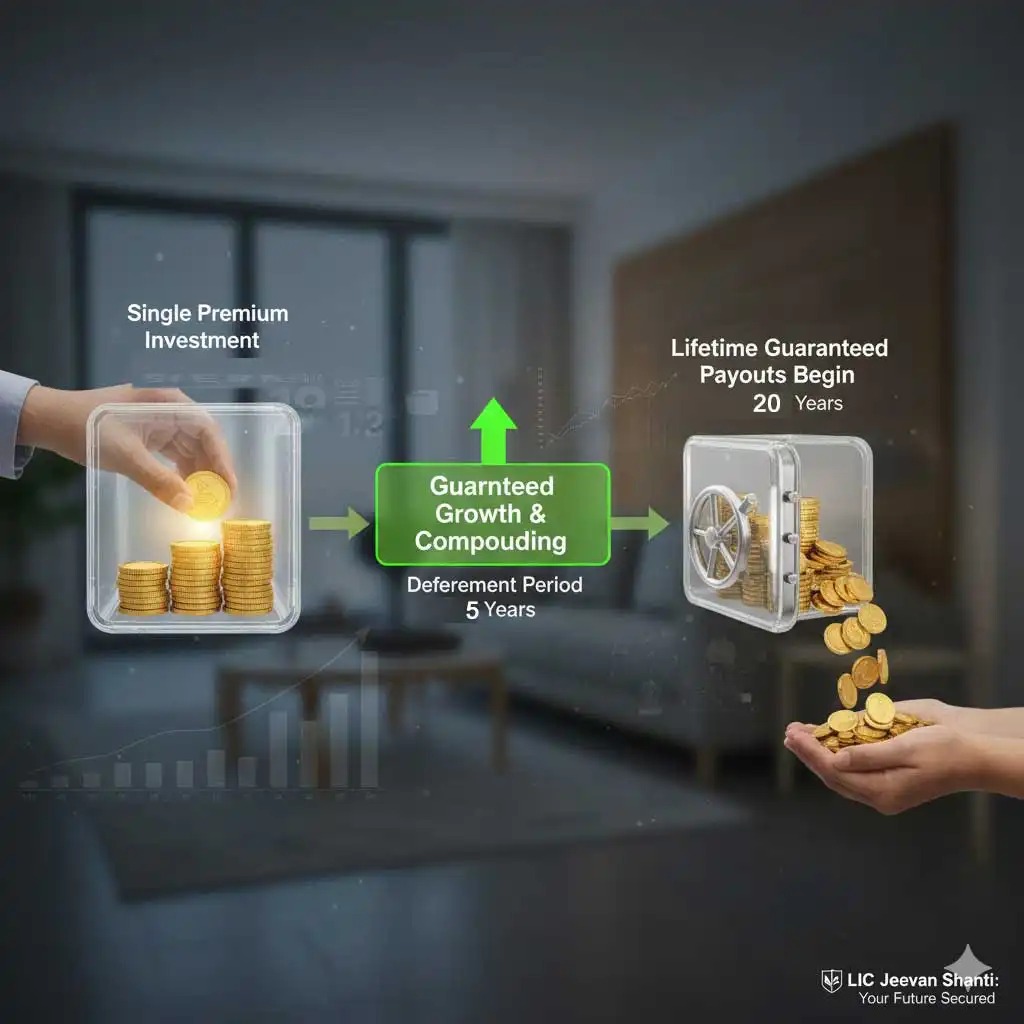

The LIC Jeevan Shanti is a non-linked, non-participating, individual, single-premium plan. This means the returns are guaranteed from the very start (policy inception) and are not dependent on market performance.

The Fundamental Choice: Immediate vs. Deferred Annuity

Historically, the plan offered both, but recent versions often focus on the Deferred Annuity option. Understanding the difference is crucial for your financial strategy:

| Feature | Deferred Annuity (Primary Focus of New Jeevan Shanti) | Immediate Annuity (Available in other LIC plans like Jeevan Akshay) |

| Premium | Single, lump-sum payment. | Single, lump-sum payment. |

| Annuity Start | Starts after a Deferment Period chosen by you (1 to 5 years). | Starts immediately after the purchase/investment. |

| Purpose | Ideal for those who have a lump sum now but are not retiring immediately (pre-retirees). | Ideal for those who have just retired and need immediate income. |

| Guaranteed Benefit | Guaranteed Annuity Rate and Accrued Additional Benefit on Death during the deferment phase. | Annuity rate is fixed for life from day one. |

Two Main Deferred Annuity Options

The New Jeevan Shanti offers flexibility through two primary deferred annuity options:

- Deferred Annuity for Single Life (Option 1): The annuity (pension) is paid to the annuitant after the deferment period for as long as they are alive. The death benefit is paid to the nominee upon the annuitant’s death.

- Deferred Annuity for Joint Life (Option 2): The annuity is paid to the primary annuitant and continues to the secondary annuitant (spouse, child, parent, etc., as per rules) as long as at least one of them is alive. The death benefit is paid to the nominee only upon the death of the last survivor.

LIC Jeevan Shanti Benefits: Guaranteed Income and Death Protection

The core promise of the LIC Jeevan Shanti Plan is a lifetime of guaranteed income, but it also includes a structured death benefit.

Survival Benefits (The Pension Payout)

Once the chosen deferment period is over, the policyholder(s) start receiving the guaranteed income after retirement for their entire lifetime, as per the chosen mode (Yearly, Half-yearly, Quarterly, or Monthly).

Death Benefit Under Deferred Annuity

The plan ensures that your lump-sum investment is protected. If the annuitant (or the last survivor in a joint-life plan) dies, the nominee receives the Death Benefit, which is the Higher of:

- Purchase Price + Accrued Additional Benefit on Death (minus any annuity payments already made, if death is post-deferment)

- 105% of the Purchase Price

The “Accrued Additional Benefit” is a guaranteed monthly addition during the deferment period, effectively allowing your corpus to grow till the annuity starts.

Eligibility, Investment, and Policy Term

Securing a future with this Best Pension Plan in India is straightforward, with flexible entry and purchase price options.

| Parameter | Criteria |

| Minimum Age at Entry | 30 years (Last Birthday) |

| Maximum Age at Entry | 79 years (Last Birthday) |

| Minimum Deferment Period | 1 year |

| Maximum Deferment Period | Up to 5 years (Subject to Max Vesting Age) |

| Maximum Vesting Age (Annuity Start) | 80 years (Last Birthday) |

| Minimum Purchase Price | ₹1,50,000 (Subject to minimum annuity limits) |

| Maximum Purchase Price | No limit |

| Minimum Annuity | ₹12,000 per annum (₹1,000 per month) |

Note: A lower minimum purchase price (e.g., ₹50,000) may apply if the policy is purchased for the benefit of a dependent person with a disability (Divyangjan).

Who Should Buy LIC Jeevan Shanti?

The LIC Jeevan Shanti Pension Plan is a versatile instrument suitable for various individuals:

- Pre-Retirees (Age 45-60): Individuals who have a lump-sum amount (from maturity of other policies, sale of asset, or gratuity) but have a few years left until actual retirement. They can opt for a Deferred Annuity to let their corpus grow with guaranteed additions before income begins.

- Retired Individuals (For Immediate Needs): Those who need a fixed income immediately can opt for the Immediate Annuity variant (if available, or consider LIC’s Jeevan Akshay VII).

- Individuals Seeking a Second Pension: People who already have other retirement savings but want a completely risk-free, guaranteed income source to cover basic expenses in old age.

- Parents Planning for Children’s Future: The joint-life option is excellent for ensuring the financial security of a spouse or lineal descendant/ascendant.

- Caregivers for a Disabled Dependent: Special provisions make this plan an ideal choice for securing the future of a dependent with a disability (Divyangjan).

Understanding Returns: LIC Jeevan Shanti Annuity Calculator & Illustration

The return under Jeevan Shanti is expressed as an Annuity Rate (pension amount per ₹1,000 of Purchase Price). This rate is guaranteed at inception.

While an accurate, personalized rate requires using the official LIC Annuity Calculator, here is a general illustration based on recent product features to demonstrate the high return and the benefit of deferment:

Illustration for Deferred Annuity (Single Life)

| Parameter | Value |

| Purchase Price (Single Premium) | ₹25,00,000 |

| Age at Entry | 45 Years |

| Deferment Period | 5 Years |

| Vesting Age (Annuity Start) | 50 Years |

| Annual Annuity Rate (Illustrative) | Approx. 8.64% |

Estimated Guaranteed Annual Pension from Age 50:

₹25,00,000 X (Approx. 8.64% = ₹2,15,875 per annum (approx.)

- Note: Annuity rates are typically higher for longer deferment periods, higher ages, and higher purchase prices (incentives).

- This illustration is indicative. Actual rates must be checked on the LIC website or via a licensed agent.

Tax Benefits of LIC Jeevan Shanti

Understanding the tax implications is vital for maximizing your retirement savings:

- Premium Payment (Investment): The single premium paid for the purchase of the LIC Jeevan Shanti is generally eligible for a deduction under Section 80C of the Income Tax Act, 1961, up to the overall limit of ₹1.5 lakh per financial year.

- Annuity Income (Pension): The annuity (pension) received regularly is considered as income and is taxable as per the policyholder’s prevailing income tax slab.

- Death Benefit: The lump-sum death benefit paid to the nominee is generally tax-free under Section 10(10D) of the Income Tax Act. However, if the nominee chooses to receive the death benefit as an annuity, the subsequent annuity payments will be taxable in their hands.

Step-by-Step Buying Process

You can purchase the LIC Jeevan Shanti from an authorised agent :

- Decide Your Option: Choose clearly between Single Life or Joint Life Deferred Annuity.

- Determine Investment & Deferment: Decide the lump-sum Purchase Price you wish to invest and the desired Deferment Period (e.g., 5 years).

- Use the Annuity Calculator: Use the official LIC Annuity Calculator online or consult an agent to get the exact guaranteed annuity rate for your chosen parameters.

- Complete Application: Fill out the proposal form, providing KYC documents (ID, Address Proof, PAN Card), and bank details for annuity credit.

- Pay Premium: Make the single-lump sum premium payment.

- Receive Policy: After verification, you will receive the policy document detailing the guaranteed annuity rate and terms.

The policy also offers a Free-Look Period where you can return the policy if you disagree with the terms.

Final Thoughts: Peace of Mind with Guaranteed Income

The LIC Jeevan Shanti Plan is an indispensable tool in any robust Indian retirement portfolio. Its strength lies in its non-market-linked, guaranteed income feature, which provides an absolute safety net for your post-retirement life. While annuity income is taxable, the assurance of a fixed, lifelong cash flow, backed by the sovereign guarantee of LIC, offers a unique value proposition that is hard to ignore, especially in an uncertain economic environment. It is a true testament to responsible financial planning.

Frequently Asked Questions

What are the documents required to buy lic jeevan shanti policy?

To purchase LIC Jeevan Shanti Plan, the policyholder must provide the following types of documents:

Address Proof – This can include a driving license, passport, voter card, Aadhar card, etc.

Identity Proof – Your identity proof can be a PAN Card, Aadhar card, passport, etc.

What is the rate of GST for single premium annuity plan?

The rate of GST (Goods and Services Tax) for single premium annuity plan, such as LIC Jeevan Shanti, is 0% of the premium amount.

What are the tax benefits?

Tax benefit on premium payments: Premium payments made towards the policy may qualify for tax deductions under Section 80C of the Income Tax Act, subject to the overall limit of Rs. 1.5 lakhs. The pension received from this product is taxable according to the individual’s tax slab.

Is there any maximum limit for the investment?

No, there is no upper limit.

Looking for immediate annuity? Check out LIC Jeevan Akshay – Immediate Annuity Plan, ideal for those seeking lifelong regular income without waiting.